Understanding how loan interest rates work is essential for anyone who plans to borrow money. Whether you’re applying for a personal loan, mortgage, student loan, or credit card, the interest rate you receive will significantly impact how much you ultimately pay. Many borrowers focus only on the loan amount, but the interest rate is often the most critical factor determining long-term financial cost.

In this comprehensive guide, we will break down how loan interest rates work, what factors influence them, and most importantly, how you can lower them to save money.

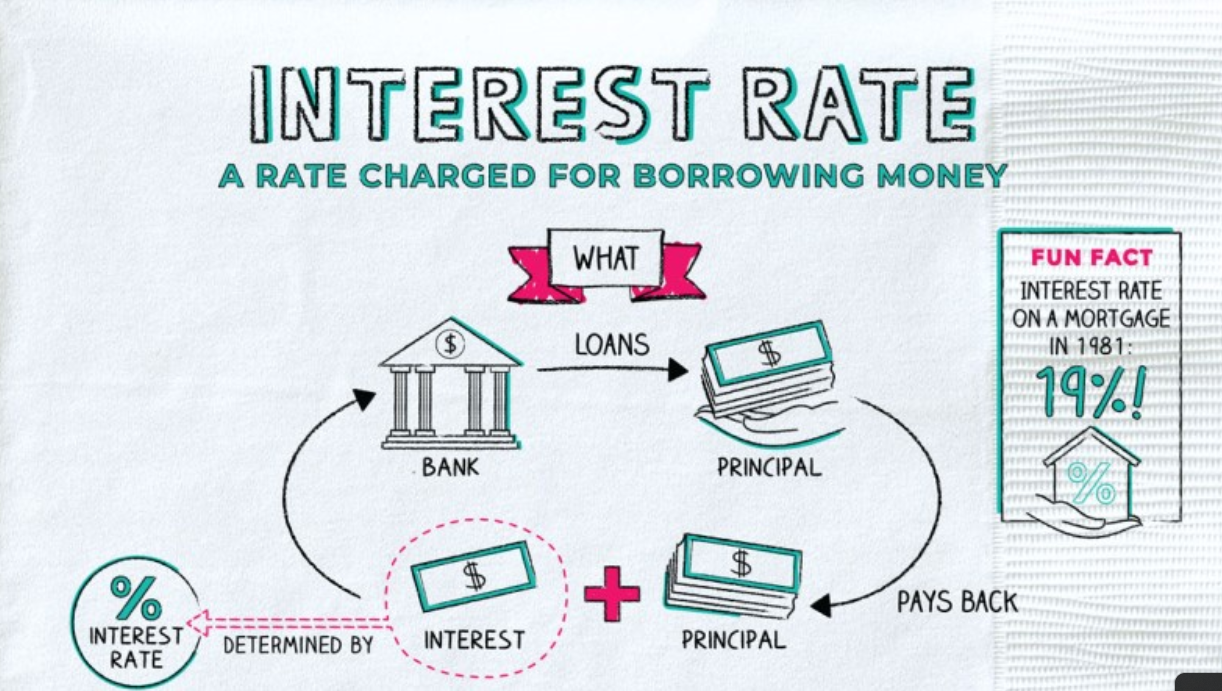

What Is a Loan Interest Rate?

A loan interest rate is the percentage charged by a lender for borrowing money. It represents the cost of using someone else’s funds and is typically expressed as an annual percentage.

For example, if you borrow $10,000 at a 10% annual interest rate, you will pay $1,000 per year in interest—assuming a simple interest structure. However, most loans use compound interest, which can increase the total cost over time.

Interest rates are how lenders make money while compensating for risk. The higher the risk of lending to a borrower, the higher the interest rate will usually be.

Types of Loan Interest Rates

Understanding the different types of interest rates helps you make better borrowing decisions.

1. Fixed Interest Rate

A fixed interest rate remains the same throughout the life of the loan. This means your monthly payments stay consistent, making budgeting easier.

Advantages:

- Predictable payments

- Protection from rising rates

Disadvantages:

- Often higher than initial variable rates

2. Variable (Adjustable) Interest Rate

A variable interest rate can change over time, usually based on a benchmark rate or index.

Advantages:

- Lower initial rates

- Potential savings if rates decrease

Disadvantages:

- Uncertainty

- Payments can increase unexpectedly

3. Simple vs Compound Interest

- Simple interest is calculated only on the principal amount.

- Compound interest is calculated on both the principal and accumulated interest.

Most modern loans use compound interest, which makes them more expensive over time.

How Loan Interest Is Calculated

Lenders use different formulas depending on the loan type, but the most common method is amortization. This means your monthly payment includes both principal and interest.

At the beginning of the loan, a larger portion of your payment goes toward interest. Over time, more goes toward reducing the principal.

This is why paying extra early in the loan term can save you a significant amount of money.

Factors That Affect Loan Interest Rates

Several key factors determine the interest rate you receive:

1. Credit Score

Your credit score is one of the most important factors. A higher score signals lower risk to lenders.

- Excellent (750+): Lowest rates

- Good (700–749): Competitive rates

- Fair (650–699): Moderate rates

- Poor (<650): High rates

2. Income and Employment Stability

Lenders want assurance that you can repay the loan. Stable income and long-term employment can help secure lower rates.

3. Loan Amount and Term

- Short-term loans typically have lower rates.

- Long-term loans may have higher rates due to increased risk over time.

4. Debt-to-Income Ratio (DTI)

This measures how much of your income goes toward debt payments. Lower DTI ratios indicate better financial health.

5. Economic Conditions

Interest rates are also influenced by broader economic factors such as inflation, central bank policies, and market demand.

6. Type of Loan

Different loans carry different risks:

- Mortgages: Lower rates (secured)

- Personal loans: Higher rates (unsecured)

- Credit cards: Highest rates

Why Interest Rates Matter So Much

Even a small difference in interest rates can lead to huge savings or costs over time.

For example:

- A 1% difference on a mortgage can mean thousands of dollars over the loan term.

- High-interest credit card debt can double what you owe if not managed properly.

Understanding this helps you prioritize getting the best possible rate.

How to Lower Your Loan Interest Rate

Now for the most important part: how to reduce the interest rate you pay.

1. Improve Your Credit Score

This is the most effective way to lower your interest rate.

Tips:

- Pay bills on time

- Reduce credit card balances

- Avoid opening too many new accounts

- Check your credit report for errors

Even a small improvement can significantly reduce your rate.

2. Shop Around and Compare Lenders

Never accept the first offer you receive. Different lenders offer different rates.

Compare:

- Banks

- Credit unions

- Online lenders

Getting multiple quotes can help you find the best deal.

3. Choose a Shorter Loan Term

Shorter-term loans typically come with lower interest rates.

While monthly payments may be higher, you’ll save money in total interest.

4. Make a Larger Down Payment

For loans like mortgages or auto loans, a larger down payment reduces risk for lenders.

Benefits:

- Lower interest rate

- Smaller loan amount

- Reduced monthly payments

5. Consider a Secured Loan

Secured loans require collateral (like a house or car), which lowers lender risk.

This often results in:

- Lower interest rates

- Better approval chances

6. Refinance Your Loan

Refinancing means replacing your current loan with a new one at a lower rate.

Best time to refinance:

- When market rates drop

- When your credit score improves

7. Use Automatic Payments

Some lenders offer interest rate discounts if you enroll in autopay.

While small (usually 0.25%), it still helps over time.

8. Reduce Your Debt-to-Income Ratio

Paying off existing debts can make you a more attractive borrower.

Lower DTI = lower perceived risk = better rates.

9. Negotiate With Lenders

Many borrowers don’t realize that interest rates are sometimes negotiable.

If you have:

- Strong credit

- Stable income

- Competing offers

You can ask lenders to match or beat a better rate.

Common Mistakes to Avoid

1. Ignoring the APR

APR (Annual Percentage Rate) includes fees in addition to interest. Always compare APR—not just interest rates.

2. Focusing Only on Monthly Payments

Lower monthly payments may mean a longer loan term and more total interest.

3. Not Reading the Fine Print

Hidden fees and variable rate clauses can increase your costs.

4. Borrowing More Than You Need

Higher loan amounts = higher interest payments.

Fixed vs Variable Rates: Which Is Better?

The answer depends on your situation:

- Choose fixed rates if you want stability and predictability.

- Choose variable rates if you expect interest rates to decrease or plan to repay quickly.

For long-term loans, fixed rates are generally safer.

The Role of Inflation and Central Banks

Interest rates are heavily influenced by inflation and central bank policies.

When inflation rises:

- Central banks increase rates

- Loans become more expensive

When inflation falls:

- Rates may decrease

- Borrowing becomes cheaper

Understanding this helps you decide the best time to borrow or refinance.

How Interest Rates Affect Different Loans

Mortgages

- Typically lower rates

- Long-term impact is significant

Personal Loans

- Higher rates due to no collateral

Credit Cards

- Extremely high rates

- Compound daily in many cases

Student Loans

- Often fixed rates

- Government loans may offer better terms

Strategies for Long-Term Savings

To minimize interest costs over time:

- Pay more than the minimum payment

- Make extra payments early in the loan term

- Refinance when possible

- Avoid unnecessary borrowing

Consistency is key to reducing financial burden.

Final Thoughts

Loan interest rates are more than just numbers—they determine how much you truly pay for borrowing money. By understanding how they work and what influences them, you can make smarter financial decisions.

Lowering your interest rate is not only possible but achievable with the right strategies. Improving your credit score, comparing lenders, choosing better loan terms, and refinancing when necessary can save you thousands of dollars.

Before taking any loan, take time to analyze all aspects—not just the amount you need, but the total cost over time. A well-informed borrower is always in a stronger financial position.