When it comes to borrowing money, choosing the right loan offer can make a significant difference in your financial future. Whether you’re applying for a personal loan, mortgage, auto loan, or business financing, understanding how to compare loan offers effectively is essential. Many borrowers make the mistake of focusing only on interest rates, but there are several other critical factors that determine the true cost and suitability of a loan.

In this comprehensive guide, you will learn how to compare loan offers step by step and choose the best deal tailored to your needs. This article is designed to be SEO-friendly, informative, and actionable so you can make confident financial decisions.

Why Comparing Loan Offers Matters

Before diving into the details, it’s important to understand why comparing loan offers is crucial. Loans can vary widely in terms of cost, flexibility, and repayment structure. Even a small difference in interest rates or fees can save—or cost—you thousands of dollars over time.

By comparing multiple offers, you can:

- Find the lowest overall cost

- Avoid hidden fees

- Choose flexible repayment terms

- Improve your financial stability

Key Factors to Compare in Loan Offers

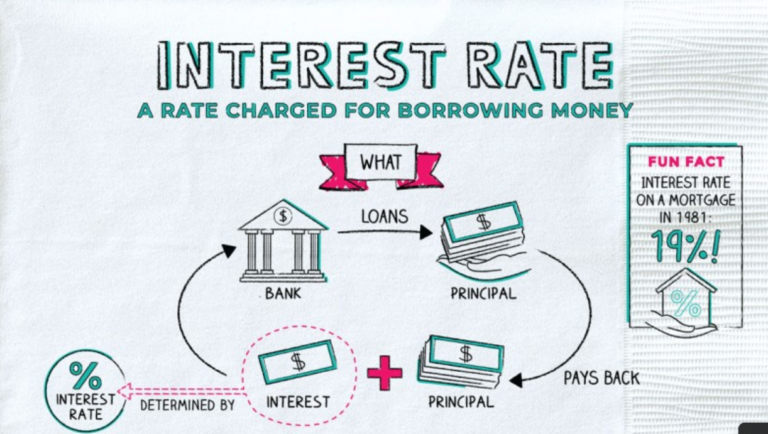

1. Interest Rate

The interest rate is one of the most important factors in any loan. It determines how much extra you will pay on top of the borrowed amount.

There are two main types of interest rates:

- Fixed Interest Rate: Remains the same throughout the loan term

- Variable Interest Rate: Can change over time based on market conditions

While a lower interest rate is generally better, it should not be the only factor you consider.

2. Annual Percentage Rate (APR)

APR provides a more complete picture of the loan cost because it includes both the interest rate and additional fees.

Always compare APR instead of just interest rates, as it reflects the true cost of borrowing.

3. Loan Term

The loan term refers to how long you have to repay the loan. It can range from a few months to several decades.

- Short-term loans: Higher monthly payments but lower total interest

- Long-term loans: Lower monthly payments but higher total interest

Choose a term that balances affordability and overall cost.

4. Monthly Payment

Your monthly payment should fit comfortably within your budget. Missing payments can lead to penalties and damage your credit score.

Use loan calculators to estimate your monthly payments before committing to a loan.

5. Fees and Charges

Many lenders include additional fees that can significantly increase the cost of the loan. Common fees include:

- Origination fees

- Late payment fees

- Prepayment penalties

- Application fees

Always read the fine print to understand all associated costs.

6. Prepayment Flexibility

Some loans allow you to pay off your balance early without penalties, while others charge fees for early repayment.

Choosing a loan with prepayment flexibility can save you money if you plan to repay the loan ahead of schedule.

7. Lender Reputation

Not all lenders are created equal. Research the lender’s reputation by reading reviews and checking ratings.

A reliable lender will offer transparency, good customer service, and fair terms.

Step-by-Step Guide to Comparing Loan Offers

Step 1: Gather Multiple Loan Offers

Start by collecting at least 3–5 loan offers from different lenders. This gives you a better perspective on what is available in the market.

Step 2: Standardize the Information

Ensure that all loan offers are based on the same loan amount and term. This makes comparison easier and more accurate.

Step 3: Compare APR First

APR is the best metric for comparing loans because it includes both interest and fees. The lower the APR, the cheaper the loan.

Step 4: Evaluate Monthly Payments

Check whether the monthly payments fit your budget. Avoid stretching your finances too thin.

Step 5: Review Fees and Fine Print

Look for hidden charges that may not be immediately obvious. These can significantly affect the total cost.

Step 6: Check Flexibility

Consider whether the loan allows early repayment, payment holidays, or refinancing options.

Step 7: Choose the Best Overall Value

The best loan is not always the one with the lowest monthly payment or interest rate. It is the one that offers the best balance of cost, flexibility, and reliability.

Common Mistakes to Avoid

1. Focusing Only on Interest Rates

Many borrowers overlook fees and APR, leading to higher overall costs.

2. Ignoring Loan Terms

A longer loan term may seem attractive due to lower payments, but it can cost more in the long run.

3. Not Reading the Fine Print

Important details about fees and penalties are often hidden in the terms and conditions.

4. Choosing the First Offer

Failing to shop around can result in missing better deals.

Tips for Getting the Best Loan Deal

- Improve your credit score before applying

- Compare offers from multiple lenders

- Negotiate terms when possible

- Consider using a loan broker

- Read all terms carefully

Tools to Help You Compare Loan Offers

There are several online tools that can simplify the comparison process:

- Loan comparison websites

- Financial calculators

- Credit monitoring services

These tools can help you make more informed decisions.

Conclusion

Comparing loan offers is a critical step in making a smart financial decision. By understanding key factors such as APR, loan terms, fees, and lender reputation, you can avoid costly mistakes and choose the best deal for your needs.

Take your time, do your research, and never rush into a loan agreement. The right choice today can save you money and stress in the future.

FAQs

What is the most important factor when comparing loans?

APR is generally the most important because it reflects the total cost of borrowing.

How many loan offers should I compare?

At least 3–5 offers to get a clear picture of the market.

Can I negotiate loan terms?

Yes, many lenders are open to negotiation, especially if you have a good credit score.

Does checking loan offers affect my credit score?

Soft inquiries do not affect your score, but multiple hard inquiries can have a small impact.