Choosing the right loan can feel overwhelming, especially with the wide range of options available today. Whether you’re planning to buy a home, start a business, pay for education, or manage unexpected expenses, selecting the right type of loan is crucial for your long-term financial health. The wrong decision could lead to unnecessary debt, high interest payments, and financial stress.

In this comprehensive guide, you’ll learn everything you need to know about choosing the right loan for your financial situation—from understanding loan types to evaluating your personal finances and comparing lenders.

1. Understanding What a Loan Really Is

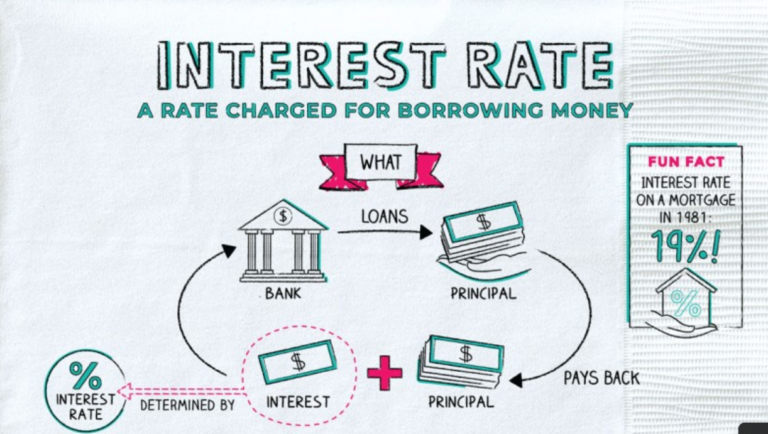

A loan is a financial agreement where a lender provides money to a borrower, who agrees to repay it over time with interest. While this sounds simple, loans come with different structures, conditions, and risks.

There are three key components of any loan:

- Principal: The amount you borrow

- Interest Rate: The cost of borrowing money

- Loan Term: The time you have to repay the loan

Understanding these basics is the foundation of making a smart borrowing decision.

2. Types of Loans Available

Before choosing a loan, you need to understand the different types available. Each loan serves a specific purpose.

a. Personal Loans

These are versatile loans that can be used for almost anything, including emergencies, travel, or debt consolidation. They are usually unsecured, meaning you don’t need collateral.

b. Mortgage Loans

Used to purchase property or real estate. These loans typically have long repayment periods and lower interest rates compared to other types.

c. Auto Loans

Specifically for purchasing vehicles. The car itself usually serves as collateral.

d. Student Loans

Designed to cover education expenses such as tuition, books, and living costs.

e. Business Loans

Used to start or expand a business. These can be secured or unsecured depending on the lender and amount.

f. Payday Loans

Short-term loans with very high interest rates. These should generally be avoided unless absolutely necessary.

3. Assessing Your Financial Situation

Before applying for any loan, you must evaluate your financial health honestly.

a. Calculate Your Income and Expenses

Understand how much money you earn and how much you spend each month. This helps determine how much you can afford to repay.

b. Check Your Credit Score

Your credit score significantly impacts your loan eligibility and interest rate. A higher score usually means better loan terms.

c. Evaluate Existing Debt

If you already have multiple loans or credit card balances, taking on more debt could be risky.

d. Determine Your Loan Purpose

Clearly define why you need the loan. Is it for a necessity or a luxury? This will guide your decision-making.

4. Secured vs. Unsecured Loans

One of the most important decisions is choosing between secured and unsecured loans.

Secured Loans

- Require collateral (house, car, etc.)

- Lower interest rates

- Higher borrowing limits

- Risk of losing assets if you default

Unsecured Loans

- No collateral required

- Higher interest rates

- Lower borrowing limits

- Less risk to personal assets

Choose based on your risk tolerance and financial stability.

5. Fixed vs. Variable Interest Rates

Fixed Interest Rates

- Remain constant throughout the loan term

- Predictable monthly payments

- Ideal for long-term planning

Variable Interest Rates

- Can fluctuate based on market conditions

- Lower initial rates but higher risk

- Suitable for short-term loans or stable economies

6. How Much Should You Borrow?

Borrowing too much can lead to financial stress, while borrowing too little might not meet your needs.

A general rule:

- Your total monthly debt payments should not exceed 30–40% of your income

Always borrow only what you truly need and can comfortably repay.

7. Comparing Loan Offers

Never accept the first loan offer you receive. Compare multiple lenders based on:

- Interest rates

- Fees and charges

- Repayment flexibility

- Customer service reputation

- Loan approval time

Use online comparison tools to simplify this process.

8. Understanding Hidden Fees

Loans often come with additional costs that borrowers overlook.

Common fees include:

- Origination fees

- Late payment fees

- Prepayment penalties

- Processing fees

Always read the fine print before signing any agreement.

9. Loan Term: Short vs. Long

Short-Term Loans

- Higher monthly payments

- Lower total interest

- Faster debt repayment

Long-Term Loans

- Lower monthly payments

- Higher total interest

- Longer financial commitment

Choose based on your cash flow and long-term goals.

10. Importance of Pre-Approval

Getting pre-approved for a loan gives you:

- A clear budget range

- Better negotiation power

- Faster final approval

It also helps identify potential issues early.

11. When to Avoid Taking a Loan

Sometimes, the best loan is no loan at all.

Avoid borrowing if:

- You don’t have a stable income

- The loan is for non-essential spending

- Interest rates are excessively high

- You’re already struggling with debt

12. Tips to Improve Loan Approval Chances

To increase your chances of approval:

- Maintain a good credit score

- Pay bills on time

- Reduce existing debt

- Provide accurate documentation

- Avoid multiple loan applications at once

13. The Role of Credit Score

Your credit score affects:

- Loan approval

- Interest rates

- Loan amount

Scores typically range from 300 to 850:

- 700+ = Good

- 750+ = Excellent

Improving your score can save you thousands in interest.

14. Online vs. Traditional Lenders

Online Lenders

- Faster approval

- Convenient process

- Competitive rates

Traditional Banks

- More reliable

- Better for large loans

- Strong customer support

Choose based on your comfort level and urgency.

15. Debt Consolidation Loans

If you have multiple debts, a consolidation loan can:

- Combine all debts into one payment

- Lower your interest rate

- Simplify finances

However, it only works if you avoid accumulating new debt.

16. Emergency Loans: What to Know

Emergency loans can help during unexpected situations, but:

- They often have higher interest rates

- Should be used only as a last resort

Building an emergency fund is always a better long-term strategy.

17. Red Flags to Watch Out For

Be cautious of:

- Lenders asking for upfront fees

- Unrealistically low interest rates

- Lack of transparency

- Pressure to sign quickly

Always verify the lender’s legitimacy.

18. How to Read Loan Agreements

Before signing, carefully review:

- Interest rate details

- Repayment schedule

- Penalties and fees

- Terms and conditions

If something is unclear, ask questions.

19. Planning Your Repayment Strategy

A solid repayment plan ensures you stay on track.

Tips include:

- Set up automatic payments

- Pay more than the minimum when possible

- Track your progress regularly

20. Final Thoughts

Choosing the right loan is not just about getting approved—it’s about making a decision that aligns with your financial goals and long-term stability.

Take your time, do thorough research, and never rush into borrowing. A well-chosen loan can be a powerful financial tool, while a poorly chosen one can lead to years of stress.

Conclusion

Finding the right loan for your financial situation requires careful planning, research, and self-awareness. By understanding different loan types, evaluating your finances, comparing options, and reading the fine print, you can make a confident and informed decision.

Remember: the best loan is one that supports your goals without compromising your financial future.